Allow Cookies ?

To enhance your browsing experience on our website, we utilize cookies. For more detailed information regarding our use of cookies, kindly refer to our privacy policy.

Allow Cookies

Allow Cookies ?

To enhance your browsing experience on our website, we utilize cookies. For more detailed information regarding our use of cookies, kindly refer to our privacy policy.

Allow Cookies

Posted On 2025-05-26

Author Shilpa Desai

Accurate financial statements are essential for determining your tax obligations.

For small and mid-sized businesses, small accounting errors—like wrong classification or missing bills—can cost you big in the form of lost deductions or extra taxes. As tax regulations evolve, authorities place a growing focus on verifying data consistency between tax returns, financial records, and third-party filings. Businesses without in-house finance teams face heightened exposure, unless their financials are meticulously structured to align with tax requirements.

This guide shows how to get your books tax-ready and bulletproof—so you can file with confidence, not just compliance.You’ll also learn how an interim CFO can support your efforts by ensuring your financials are both tax-aligned and audit-ready.

For tax purposes, your financial statements act as filters—determining what gets flagged, what gets limited, and where you're most exposed.

Your financial statements, including revenue, expenses, depreciation, and payables, are directly compared with GST filings, TDS returns, and bank records. If these records do not accurately reflect actual transactions or lack necessary supporting details, it not only increases the risk of a notice but also potentially raises your tax liability.

The goal is to ensure your records align with actual business activities. Discrepancies between your statements and third-party data can weaken your position during tax assessments. Whether it's a balance sheet that doesn’t match GST returns, a cash flow statement that omits debt information, or a profit and loss account that shows unexplained variations, these issues create potential problems when reviewed by tax authorities.

Here’s what tight financials enable you to do before filing:

Validate eligibility for deductions and depreciation with supporting schedules.

Avoid penalties due to mismatch between reported income and actual receipts.

Present clean data trails that stand up in case of scrutiny—especially for businesses nearing audit thresholds.

If your financial statements aren't prepared with tax alignment in mind from the start, you're increasing your risk without realizing it. As filings become more automated, even small mismatches across returns can lead to avoidable notices, audits, or delays.

Before any deductions are calculated or tax-saving strategies explored, the first thing that defines your liability is whether your numbers are defensible. Not rounded-off, estimated, or backed by memory—but backed by clean, timestamped, reconciled records.

For SMEs, consistency across financial statements and regulatory data isn’t optional. When internal expertise is limited, temporary CFO services can fill the gap, ensuring reconciliations and GST data are consistently aligned.

Common Triggers That Invite Scrutiny :

Unreconciled bank entries that don’t match invoice dates or amounts.

Expenses without vendor-compliant GST invoices.

Cash transactions that lack audit trails, especially in expense-heavy businesses.

Delayed or incomplete data entry in accounting systems.

Investors and tax officers look for different things, but they both rely on internal accuracy. If your P&L shows rent payments every month but there are no matching bank debits, or if depreciation is claimed without an updated asset register, you’re either leaving money on the table—or inviting assessment.

Most importantly, clean books make risk visible early. If a tax liability looks outsized for your revenue level, you’ll catch it before filing. That gives you time to correct, disclose, or plan—without triggering late fees or interest.

Tax filings rely on the accuracy of financial statements, which in turn depend on the completeness of day-to-day transaction records. Gaps or inconsistencies at the transaction level are often where compliance issues begin.

Once accuracy is in place, the next layer of tax efficiency is how your financial data is structured—because a well-organized set of books doesn’t just prevent penalties, it helps reduce the tax owed.

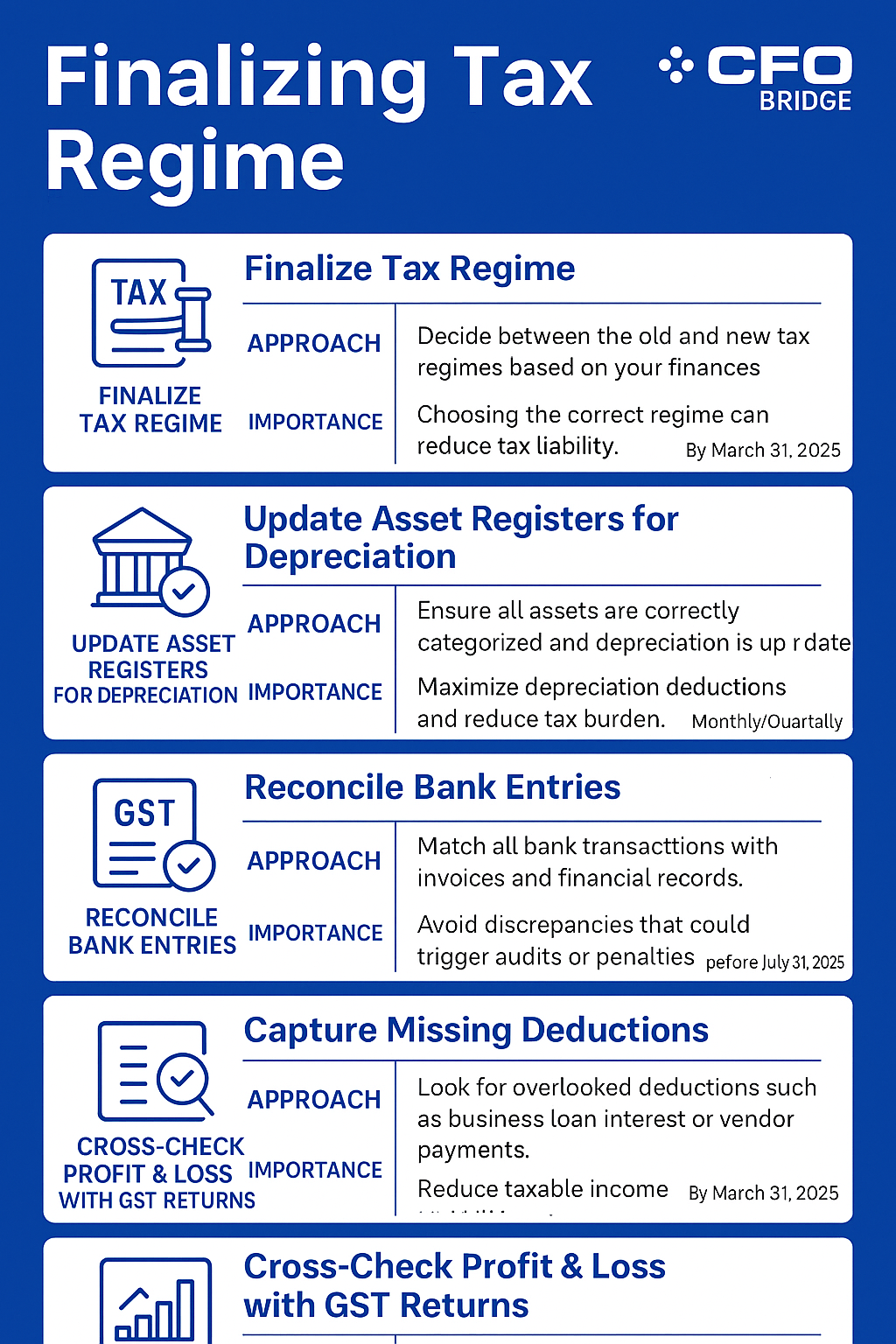

The structure of your finances determines your ability to fully claim depreciation and substantiate deductions. It also affects your selection of the tax regime that most effectively supports your business model, rather than one that simply seems more straightforward.

Start with how you approach these three decision points:

Don’t assume the new regime is always cheaper.. If your SME regularly claims depreciation, interest on business loans, or deduction-heavy expense categories, you may benefit more under the older regime—even with higher rates. But this choice only becomes clear when books are closed early enough to run side-by-side simulations.

SMEs often overlook standard deductions such as:

Depreciation on machinery or technology upgrades that goes unclaimed due to missing or poorly maintained asset registers.

Interest paid on formal business loans, including OD limits or invoice financing.

Rent, travel, or vendor payments that weren’t booked against proper invoices. These aren’t loopholes—they’re standard deductions left behind due to incomplete documentation or vague categorization in accounts.

ITC claims are frequently challenged during GST scrutiny, particularly when discrepancies exist between your supplier’s return and your own. To ensure these claims are secure:

Ensure all vendors are GST-compliant.

Cross-check GSTR-2B regularly.

Reconcile ITC claimed in books with monthly filings—before the financial year closes.

These steps are essential. Failing to address them before finalizing your statements can result in overpayments and the persistence of inefficiencies that escalate over time.

Filing on time doesn’t guarantee tax efficiency. That’s why many growing SMEs rely on interim CFO services to finalize books in advance and ensure filing posture is proactive rather than rushed.

When financial decisions are made reactively, the tax impact is locked in before filings even begin.

Deadlines are fixed. But your filing posture—whether it’s defensive, proactive, or simply rushed—is a result of how early your internal numbers are finalized.

Here’s what structured filing discipline enables:

Room for Strategic Regime Selection: The earlier your financials are finalized, the more flexibility you have to model tax outcomes, compare regimes, and make deliberate decisions. When finalization is left to the last minute, filing becomes reactive—leaving little room for optimization or error correction.

Better Audit Readiness: When books are closed in phases (quarterly or monthly), there’s less year-end compression. That means fewer inconsistencies, cleaner documentation, and reduced stress if you’re selected for review.

ITC and GST Alignment: Monthly GST returns don’t just affect compliance—they influence how much input credit you can legally retain. Delays or mismatches lead to blocked ITC, which directly increases your working capital outflow. Aligning internal books with GSTR-2B monthly saves that cost.

Smoother Advance Tax Handling: Many SMEs underestimate their income, miss advance tax milestones, and end up paying interest. A quarterly profit snapshot lets you forecast liability more accurately and spread tax payments—without last-minute shocks.

Late filing is costly. Timely filing with messy books? Even worse. The only filings that actually protect your margins are the ones backed by structured, reviewed, and reconciled numbers—weeks before the deadline, not days.

For SMEs without in-house finance teams, partnering with CFO Bridge can provide the strategic insights and document preparation needed—whether through shared CFO services, temporary CFO services, or full-spectrum support from an experienced fractional CFO.

Getting your books right from the start is key to controlling liability and minimising tax impact. The earlier you align your financials, the easier it becomes to manage taxes as part of your growth strategy rather than a burden.

If your team needs support in preparing year-end financials for tax filing, CFO Bridge offers structured assistance focused on accuracy, compliance, and timely reporting. Our services are designed to match the pace and requirements of SMEs—whether it's for a single filing cycle or recurring support.

Look for: A mismatch between turnover declared in ITR and GST returns Large jumps in expense categories without matching revenue movement A sudden drop in profit despite stable revenue High cash transactions or unusual ledger balances (e.g., loan entries, sundry creditors) These don’t guarantee a notice, but they raise your audit probability. An internal review by a tax consultant can flag risks early.

Yes, certain corrective actions can still help reduce your liability—such as updating asset registers for accurate depreciation claims, verifying full input tax credit (ITC) capture, and reconciling capital accounts. However, the most effective tax strategies are implemented before March 31, not after. For the next financial year, shift to quarterly alignment of your books to gain better control over outcomes—not just reactive adjustments in March.

Many SMEs manage well with fractional CFOs, freelance accountants, or CA retainers, provided roles are clearly defined. Compliance doesn’t require full-time staff—it requires consistent oversight. What matters is not internal headcount, but whether someone is actively tracking deadlines, reconciliations, and reporting gaps.

You should target the closure of draft financials by early May, even though the deadline is July 31 (or October 31 for audited entities). Early closure allows time for regime simulations, correction of entries, GST reconciliation, and audit prep (if required). Last-minute closures almost always lead to missed deductions or avoidable errors.

Answer a few questions and get matched with experts who’ve helped 500+ businesses like yours.

CEO Description

Here's a curated list of finance leaders for your industry and company size.

Finding your perfect CFO partners...

Our talented team will reach you out shortly.

Let's talk! Book your free consultation today